This article explains the 2000 IRS direct deposit update, the payment schedule starting January 18, the rules that affect who gets paid, and what you should do right away. Read the steps carefully to avoid delays or scams.

What the 2000 IRS Direct Deposit Update Means

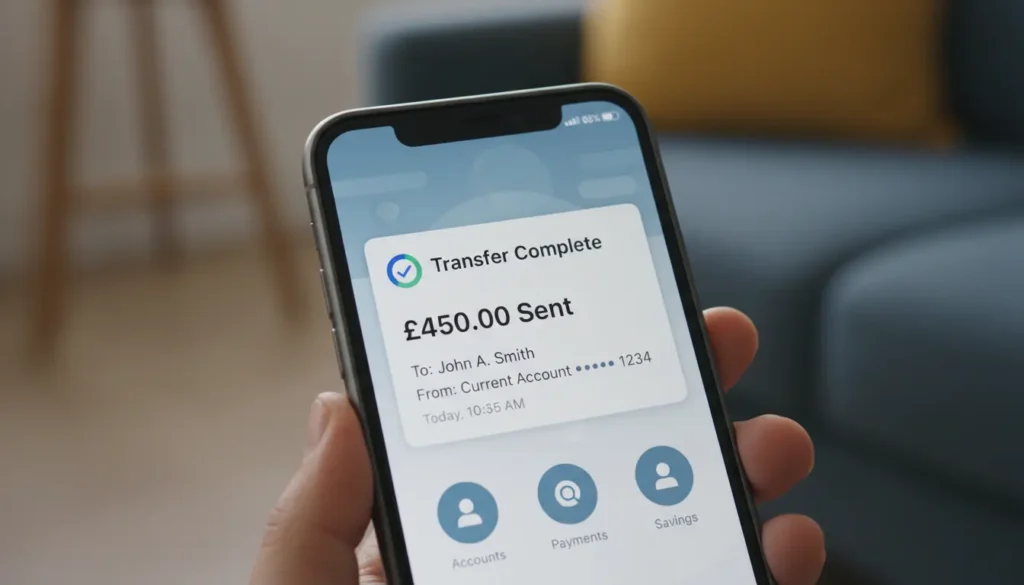

The update refers to new direct deposit payments of 2000 that the IRS has scheduled to begin on January 18. These deposits are being sent electronically to eligible recipients in batches over several days.

Not everyone will receive a deposit on the first day. The IRS usually staggers direct deposits based on bank processing windows and eligibility checks.

Payments Starting January 18: Timing and Expectations

Payments starting January 18 will appear as direct deposits in bank accounts that the IRS already has on file. Banks can take one to three business days to post the deposit after the IRS sends it.

Key expectations:

- Deposits may show as an unlabeled ACH credit in your account — check recent transaction details carefully.

- Some people will get mailed checks or prepaid debit cards instead of deposits depending on IRS records.

- If you usually get your tax refund by direct deposit, the IRS will likely use the same bank routing and account number on file.

Who Is Likely Eligible

Eligibility is determined by IRS rules for the specific payment program. Typical factors include recent tax filings, reported income, and dependent status.

If you filed taxes or a non-filer submission in the last relevant tax season, the IRS will use that information to decide eligibility and the payment destination.

Rules to Know About the 2000 IRS Direct Deposit Update

Understand these rules so you can act quickly and avoid common pitfalls.

- Eligibility is based on IRS records: If your bank account or address has changed, the IRS may not be able to deposit funds.

- Payments are final: If a deposit goes to a closed or incorrect account, the money may be returned to the IRS and then reissued by mail, causing delay.

- Watch for notices: The IRS will often send letters explaining deposits or next steps. Keep any official mail.

- Watch out for scams: The IRS will not call demanding payment information to send a deposit. Verify any contact you receive.

What to Do Immediately

If you believe you should receive a 2000 direct deposit, take these immediate steps. Acting now reduces the risk of delays or lost funds.

- Check your bank account online and transaction histories for unexpected ACH credits starting January 18.

- Review your most recent tax return or non-filer submission to confirm the bank routing and account number the IRS has on file.

- Sign in to official IRS tools (for example, the IRS account portal) to see payment status and messages. Only use IRS.gov links.

- If your bank information changed since your last IRS filing, prepare to file an update with your next tax return and monitor for mailed payment options.

- Keep an eye out for an official IRS letter explaining the payment. Save it for your records.

How to Verify a Deposit Safely

Use your bank app or official IRS resources. Do not provide personal data in response to unsolicited calls, texts, or emails.

Steps to verify:

- Check the exact ACH entry; note the sender name and amount.

- Log in to IRS.gov to check payment status if the site offers a specific portal for the payment type.

- If you suspect a problem, call your bank using the number on the back of your card — not a number from an email or text.

The IRS sometimes reissues electronic payments as paper checks when a direct deposit cannot be completed. That shift can add several weeks to delivery time.

If You Do Not Receive a Deposit

Not receiving a deposit on or after January 18 does not necessarily mean you are ineligible. The IRS processes payments in waves and may issue a mailed check later.

If you suspect an error, gather relevant documents before contacting the IRS or your bank. These include your most recent tax return and bank statements.

When to Contact the IRS or Your Bank

- Contact your bank if the deposit appears in pending transactions but is not posted after three business days.

- Contact the IRS only after confirming that your records show eligibility and the bank account on file is correct, and if the IRS payment tracker confirms a problem.

Real-World Example

Case Study: Maria, a single parent and part-time worker, expected the 2000 payment. She checked her last tax return and confirmed the direct deposit account on file. On January 19 she saw an unlabeled ACH deposit for 2000 appear as pending in her bank app.

Maria waited two business days for the bank to clear the funds. When the deposit posted, she received an IRS notice in the mail explaining the deposit. Because she had saved the notice and bank record, there was no delay resolving a minor labeling confusion with her credit union.

Common Questions and Quick Answers

Q: Will the IRS ever call to confirm my bank account for a deposit? A: No. The IRS will not call to ask for banking information to send a payment.

Q: What if the deposit is incorrect? A: Save all documentation and contact the IRS using phone numbers on IRS.gov. Your bank can also advise on returned funds.

Final Practical Checklist

- Check your account starting January 18 for an ACH credit.

- Confirm the bank info the IRS has on file from your last filing.

- Use IRS.gov and your bank app only; ignore unsolicited contact.

- Save IRS letters and bank statements if a payment posts to your account.

- Contact the bank first for posting issues, then the IRS if records show an error.

Following these steps will help you recognize a legitimate 2000 IRS direct deposit, act quickly if something goes wrong, and protect your personal information from scams. Stay organized, verify with official sources, and save documentation until the payment is fully resolved.