Overview: What the New 725 Guaranteed Income Plan Is

The New 725 Guaranteed Income Plan provides eligible U.S. households with regular payments of up to $725. This article explains the program, who qualifies, how payments arrive, and what families should do now.

How the New 725 Guaranteed Income Plan Works

The program guarantees a base payment that varies by household size and income. Most eligible households will receive monthly payments designed to supplement earnings and reduce economic insecurity.

Key program features

- Maximum benefit: $725 per month for qualified households (amounts scale by household size).

- Delivery: Payments are sent monthly through direct deposit or a prepaid card option.

- Duration: Initial rollout covers 12 months; extensions may be decided later.

Who Qualifies for the 725 Guaranteed Income Plan

Eligibility rules focus on residency, income, and family composition. States and federal rules may both apply depending on where you live.

Common eligibility criteria

- U.S. citizen or lawful resident and primary residence in participating area.

- Income below a set threshold (typically tied to area median income or federal poverty levels).

- Prioritization for households with children, seniors, or people with disabilities.

Check your state or locality’s portal for the exact income limits and documentation required.

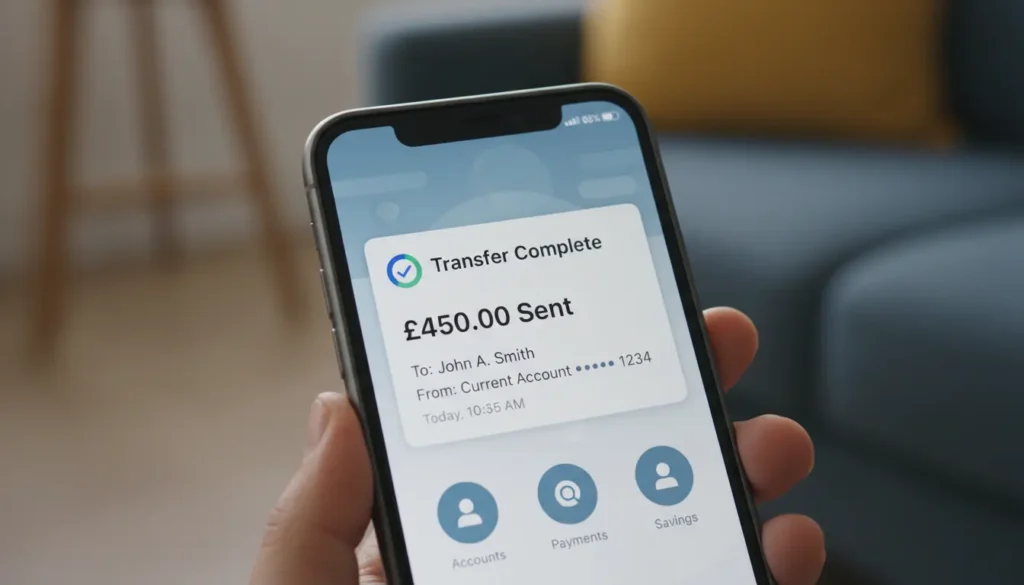

How and When Payments Arrive

Payments usually begin after the application window closes and identity checks are complete. Expect an initial verification period of 4–8 weeks.

Delivery methods

- Direct deposit to a bank account (fastest option).

- Prepaid debit card mailed to the recipient (for those without bank accounts).

- Paper checks in limited cases or where other methods aren’t available.

Keep your contact and banking information updated in the program portal to avoid delays.

Tax and Benefit Interactions for the 725 Guaranteed Income Plan

Most guaranteed income payments are considered taxable income at the federal level unless the program states otherwise. State tax rules vary.

What to watch for

- Report the payments on your federal tax return unless the program is explicitly non-taxable.

- Some means-tested benefits (SNAP, TANF, housing assistance) could be affected; the program may exclude payments from benefit calculations in some states.

- Keep program statements and annual tax forms for accurate reporting.

How to Apply and What Families Should Do Now

Applying typically requires an online form, proof of identity, proof of residence, and income documentation. Many local agencies offer phone or in-person help.

Step-by-step actions

- Find your state or local program page and read eligibility details.

- Gather documents: ID, utility bill, pay stubs or tax return, and proof of household size.

- Apply online or use a community partner (libraries, non-profits) for help with the application.

- Sign up for direct deposit to receive payments quickly and securely.

- Save copies of confirmation emails or application receipts.

Apply as early as possible. Limited funding or caps on household enrollment may mean earlier applicants are prioritized.

Some pilot programs that paid families small monthly amounts showed measurable increases in food security and reduced emergency borrowing within six months.

Practical Budgeting Tips When You Receive 725 Guaranteed Income Payments

Use the payments to cover recurring needs and build short-term stability. Treat the money as flexible but plan to make it count.

- Create a simple budget: allocate for rent, utilities, groceries, and emergency savings.

- Set up automatic transfers to a savings account on payment day to build a small safety net.

- Use one-time portions for essential repairs or replacing broken items that reduce ongoing costs.

Small Real-World Case Study

Maria is a single parent in Columbus, Ohio, working part-time and caring for two children. Her household income qualified her for the New 725 Guaranteed Income Plan.

Before the program she relied on irregular gig work to cover bills. After enrolling, Maria received $725 monthly and used it to stabilize rent payments and set aside $50 per month in savings.

Within three months she avoided an eviction notice, paid down a small medical bill, and increased grocery stability for her family. She reported lower stress and fewer late notices, which improved her credit interactions.

Common Questions Families Ask About the 725 Guaranteed Income Plan

- Will the money affect my other benefits? Possibly. Check your benefit agency; some programs exclude guaranteed income from counts.

- Do I need to repay it? No, these are payments, not loans.

- What documentation is permanent? Keep tax forms and program notices at least three years for tax and audit purposes.

Where to Find Official Information

Start with your state government website or local social services office. National agencies and non-profits often publish plain-language guides and helplines.

Check for updates regularly, because eligibility rules and rollout schedules can change as the program expands or receives additional funding.

Next Steps for U.S. Families

Confirm eligibility, apply quickly, and prepare to document income and residency. Use the payments intentionally to stabilize monthly needs and build a small emergency fund.

If you need help applying, contact local community organizations or your state benefits office. Many places offer free application support and translation services.

Keeping records and planning for tax reporting will make the program easier to manage and reduce surprises at tax time.